Even though the first significant uptick in ransomware attacks began over three years ago, a steady increase in frequency and severity has likely now made ransomware exploits the number one security threat faced by most businesses today. McAfee places the ransomware growth rate for the last quarter at 118%. Many smaller businesses were previously on notice but chose to ignore the warning signs. Thankfully, after the 2017 ransomware attacks unleashed by the Wannacry strain of Cryptolocker, some companies did address ransomware risk by implementing better employee training while others decided to upgrade legacy software and initiate offsite backups.

Those who did not adequately address this risk, however, are now facing much larger extortion demands. Also, the risk landscape has changed dramatically over the past several years with ransomware becoming an equal opportunity attack that will now target local governments as well as dental offices. Indeed, even first grade students are now being impacted by network security intrusions that not too long ago only previously targeted only large universities.

Despite the recent public trend of paying these extortion demands, the FBI has long advocated not paying a ransom in response to a ransomware attack. Specifically, the FBI has said: “Paying a ransom doesn’t guarantee an organization that it will get its data back—we’ve seen cases where organizations never got a decryption key after having paid the ransom. Paying a ransom not only emboldens current cyber criminals to target more organizations, it also offers an incentive for other criminals to get involved in this type of illegal activity. And finally, by paying a ransom, an organization might inadvertently be funding other illicit activity associated with criminals.”

In fact, some have argued that by having insurance for this exposure the industry itself is actually at the root of increased ransomware activity. Those in the security industry correctly point out that what drives these actors turns more on quick conversion rates rather than whether an insurer stands behind a victim. To suggest the insurance industry is the cause of this problem gives threat actors way too much credit while completely ignoring the benefits derived from the cyber insurance underwriting process.

In the same way it is never too late to go back to school, it is never too late to begin importing a more robust security and privacy profile into an organization – which is the only real way to diminish the risk of a ransomware attack. As suggested in 2016: “Given the serious threat of ransomware, businesses large and small are reminded to at least do the basics – train staff regarding email and social media policies, implement minimum IT security protocols, regularly backup data, plan for disaster, and regularly test your plans.”

On July 24, 2019, the FTC filed its Stipulated Order requiring that Facebook comply with newly-imposed privacy requirements for a period of twenty years. The most noteworthy aspect of this Order, however, does not relate to the specifics of this compliance framework – which can easily be addressed with the right counsel. Rather, the requirement that is more challenging for Facebook is the one creating an “Independent Privacy Committee” within Facebook’s Board of Directors “consisting of Independent Directors, all of whom” have “(1) the ability to understand corporate compliance and accountability programs and to read and understand data protection and privacy policies and procedures, and (2) such other relevant privacy and compliance experience reasonably necessary to exercise his or her duties on the Independent Privacy Committee.”

Such specific requirements regarding the capabilities of a Board member are more than a bit unusual. Given the fiduciary responsibilities of Board members as well as the reputations of those willing to become members of this “Independent Privacy Committee”, this novel requirement may actually do something to curtail future privacy transgressions.

There is no doubt the FTC resolution was Facebook’s well-orchestrated attempt at rehabilitating its tattered reputation. As stated in Facebook’s blog response: “Billions of people around the world use our products to make their lives richer and to help their organizations thrive. That makes it especially important that the people who use our platform can trust that their information is protected. This agreement is an unambiguous commitment to do that.” Indeed, this agreement may even be marketed as a way of bolstering dwindling user engagement.

Facebook’s regulatory problems are far from over – the DOJ just announced a wide-ranging antitrust probe that includes Facebook. Specifically, the Department of Justice’s Antitrust Division will review “whether and how market-leading online platforms have achieved market power and are engaging in practices that have reduced competition, stifled innovation, or otherwise harmed consumers.” This antitrust probe will likely end up being much more interesting and potentially damaging to Facebook than the recent FTC settlement – especially depending on what road is taken by its potential privacy-killing Calibra business unit.

Using a tone that permeated for much of the hearing, Sen. John Kennedy ignored Facebook’s participation in a Swiss Association that purportedly leaves Facebook with little control over Libra and instead mocked: “Facebook wants to control the monetary supply. What could possibly go wrong?” Sen. Sherrod Brown (D-OH) reinforced this lack of trust when he said that Facebook was dangerous because it did not “respect the power of the technologies they are playing with, like a toddler who has gotten his hands on a book of matches, Facebook has burned down the house over and over, and called every arson a ‘learning experience.'”

Sen. Brian Schatz summed up the mood nicely when he recognized: “You’re making an argument for cryptocurrencies generally. The question is not, ‘Should the U.S. lead in this?’ Why in the world, of all companies, given the last couple of years, should [Facebook] do this?”

On a more substantive side, the hearing was driven by a concern for privacy rights. As reported in The Wall Street Journal, Mr. Marcus suggested that Facebook would not monetize users’ data related to Libra because no financial or account data from the Libra network would be shared with Facebook: “We’ve heard loud and clear from people, they don’t want those two types of data streams connected.”

Even though it did not garner much public analysis, Chairman Crapo’s Statement provides an important privacy perspective that may also set the table for future legislative action: “Individuals are the rightful owners of their data. They should be granted a certain set of privacy rights, and the ability to protect those rights through informed consent, including full disclosure of the data that is being gathered and how it is being used.”

And, despite all of his protestations to the contrary, in his own prepared testimony, Mr. Marcus actually provides a rough roadmap detailing how the financial and transactional data obtained by Calibra could directly bolster Facebook’s data surveillance revenue.

Specifically, Mr. Marcus states: “The Calibra wallet will let users send Libra to almost anyone with a smartphone, similar to how they might send a text message, and at low-to-no cost. We expect that the Calibra wallet will ultimately be one of many services, and one of many digital wallets, available to consumers on the Libra network. We do not expect Calibra to make money at the outset, and Calibra customers’ account and financial information will not be shared with Facebook, Inc., and as a result cannot be used for ad targeting. Our first goal is to create utility and adoption, enabling people around the world— especially the unbanked and underbanked—to take part in the financial ecosystem. But we expect that the Calibra wallet will be immediately beneficial to Facebook more broadly because it will allow many of the 90 million small- and medium-sized businesses that use the Facebook platform to transact more directly with Facebook’s many users, which we hope will result in consumers and businesses using Facebook more. That increased usage is likely to yield greater advertising revenue for Facebook.”

To suggest that the mere ancillary use of Facebook’s platforms by Calibra users will alone cause an increase in advertising revenue makes little sense. The only way Calibra will yield greater “advertising revenue” to Facebook is directly related to the well-understood increase in value user data would have after alignment takes place between transaction data and the other data obtained from Facebook’s platforms and services. Indeed, advertisers have long recognized that personalization data is not nearly as useful as relevance data.

A long-term goal of Facebook’s Libra project, namely combining user data with associated financial and transactional data, should not be considered well-hidden. Mr. Marcus’ written testimony all but confirms Facebook will eventually harvest transactional and KYC data: “Calibra will not share customers’ account information or financial data with Facebook unless people agree to permit such sharing.” Indeed, Sen. Pat Toomey specifically asked Mr. Marcus whether Facebook intended to seek user consent to monetize Calibra-derived financial data and Mr. Marcus incredibly responded: “I can’t think of any reason right now for us to do this.” Really?

House Financial Services Committee Hearing of July 17, 2019

One major difference between the Senate hearing conducted on July 16, 2019 and the House Financial Services Committee hearing of July 17, 2019 was the sort of testimony provided by industry experts. Even though the Senate smartly sought testimony from Wall Street and blockchain industry expert Caitlin Long, unlike with the House, there were no one educating the Senate on Calibra’s privacy issues.

For example, MIT Professor Gary Gensler’s prepared House testimony lays out a number of questions regarding privacy that Facebook should answer at some point: “We know that many of the most intrusive privacy practices of concern to privacy regulators have actually been subject to some form of consumer consent. So, it will be essential to conduct a more thorough analysis of what uses of Libra data should be allowed and which uses should be prohibited. How would such restrictions be monitored and enforced? What are the limited exceptions and might Calibra broadly seek customer consent in the form of standard user agreements? It would be likely that Calibra would want to commercialize this data. At a minimum, without sharing the raw transaction data from customers’ Calibra Wallets, it would still likely analyze such data to earn money either through advertisements or by offering targeted services to wallet holders.”

As well, in the prepared written testimony of Robert Weissman, President of Public Citizen, there is a long discussion explaining why Facebook is a “Corporate Surveillance Leviathan” that cannot be trusted with the proposed Calibra wallet.

The House Hearing also raised the issue of whether Facebook would be able to pick and choose users of the Calibra wallet – potentially forcing persons to conform their behavior to Facebook standards. In one highlight of the House Hearing, Congressman Sean Duffy waved a twenty-dollar bill in the air while making the point that anyone, including persons who say horrible things, can use a twenty-dollar bill but: “Who can use Calibra?” In response, Mr. Marcus pointed out anyone who could satisfy Calibra KYC requirements – which then begged the loaded follow-up question from Congressman Duffy: “Could Milo Yiannopoulos and Louis Farrakhan use Calibra [given they are both banned from Facebook]?” In response, Mr. Marcus said that an applicable policy hasn’t yet been written but that it was “an important question that [Facebook] needed to be thoughtful about.”

Given Facebook’s poor track record – indeed, former Facebook executives readily acknowledge Facebook holds too much market power and should not be trusted going forward, these and other “important questions” must be answered as soon as possible.

According to the ICO, the massive fine was ultimately based on the harvesting of personal data of approximately 500,000 customers only one month after GDPR became enforceable. The ICO investigation uncovered that “a variety of information was compromised by poor security arrangements at the company, including log in, payment card, and travel booking details as well name and address information.”

Given that the ICO’s final decision will take into consideration a formal response from British Airways and other data protection authorities, the fine will likely be modified in same way – this is also likely given there were new security procedures implemented by British Airways, there is no present evidence of fraud, and British Airways has already threatened an appeal.

At the time of the attack, British Airways provided very little information regarding how it was accomplished other than to say it impacted website and app bookings from August 21 to September 5, 2018 and that it was the victim of a “sophisticated, malicious criminal attack“. One security expert posited that malicious code was planted on the website’s payments page using a modified version of the Modernizr JavaScript library. Others have considered this attack caused by a cross-site scripting exploit. No matter what the attack vector or exploit, this was clearly the sort of security lapse that has dogged many companies over the years. To now have a potential $229 million fine waiting on the sidelines can only be considered yet another massive motivation to get one’s security house in order as soon as possible.

Facebook’s crypto advertising ban and duopolistic reach pretty much sums up why potential users should be careful before jumping on the Libra bandwagon. In what can only be considered ironic, the “Libra Coin” is not even a true cryptocurrency or even built on a blockchain – it is apparently the token for a permissioned payment network that is partially decentralized while requiring the disclosure of sensitive authentication data as well as use of the Calibra wallet owned and operated by Facebook itself. Most importantly, as a node on the network Facebook will also have access to all consumer transaction data flowing on the network. Like icing on a global cake, by being part owner of a de facto bank, Facebook will also get to share in any float interest.

Those premier venture firms and companies who have anted up to align with Facebook’s project may believe in the collective end game but to align now with Facebook simply because of its tremendous reach will likely be a mistake for them as well as the consuming public.

On June 6, 2019, Maine joined a chorus of state legislatures moving on data privacy – this time requiring providers of broadband Internet services to obtain express consent before using a consumer’s personal information. Specifically, the new Maine law reads: “A provider may use, disclose, sell or permit access to a customer’s customer personal information if the customer gives the provider express, affirmative consent to such use, disclosure, sale or access. A customer may revoke the customer’s consent under this paragraph at any time.”

Maine’s law is even more restrictive than California’s Consumer Privacy Act which will deploy an “opt out” mechanism requiring the consumer to inform data processors of their preference. Both Californians and Mainers will have to wait until 2020 to benefit from their respective data privacy laws – with the Maine statute taking effect on July 1, 2020.

As reported in The Hill, tech lobbyists are now exerting their best efforts on obtaining a federal law that will moderate this and other consumer privacy state gains – which is not surprising given even stricter data privacy laws percolating in other states. Whether or not certain data privacy provisions die in a preemption skirmish, data rights will continue their reimagination by market forces so lobbyists alone can never prevail in their clients’ war against true individual data ownership.

New York now is now moving on a bill, S5642, that is even more protective than the California Consumer Privacy Act while New Jersey is in the process of merging two proposed bills that may lead in the same direction. There has been opposition to these proposed laws by those companies who have the most to lose by stringent data privacy controls.

If passed, however, these new laws may actually prod Congress to finally move on a comprehensive privacy framework – one that might preempt aggressive laws such as the ones proposed by New York and New Jersey and the one already passed in California, in favor of a much more tempered approach.

In other words, the Internet Association and its lobbying partners may actually win the war if these bills are enacted and it can just get Congress to act in a preemptive manner. Thankfully, the momentum has been consistently on the side of consumer protection and any hope of bipartisan action on the part of Congress remains a long-shot given the current political environment.

On May 6, 2019, the Office for Civil Rights (OCR) announced that Tennessee-based Touchstone Medical Imaging agreed to pay $3,000,000 and adopt a corrective action plan that includes the adoption of business associate agreements, completion of an enterprise-wide risk analysis, and additional comprehensive policies and procedures applying HIPAA Rules. Touchstone – which provides diagnostic medical imaging services, was notified in May 2014 by the FBI that one of its FTP servers allowed uncontrolled access to protected health information (PHI). This uncontrolled access “permitted search engines to index the PHI of Touchstone’s patients, which remained visible on the Internet even after the server was taken offline.”

During OCR’s investigation, Touchstone acknowledged that the PHI of more than 300,000 patients was exposed including, names, birth dates, social security numbers, and addresses. OCR’s investigation found that Touchstone “did not thoroughly investigate the security incident until several months after notice of the breach”. As a result, Touchstone’s notification to individuals affected by the breach was considered untimely.

Given last year’s summary judgment win by OCR and the facts presented by the Touchstone incident, it is not surprising that this significant settlement – which was one of the largest to date, was reached. FTP servers have long been a threat vector – even if set up and run properly, so not unlike the clarion calls initiated for encryption and social engineering training, back office IT support should be sophisticated enough to adopt a means of file transfer that applies state of the art security.

Whether Facebook survives as a social media platform may eventually hinge on a metric that has not been widely reported – which is ironic given what has recently been reported is hardly good news.

Almost comically, on April 29, 2019, Facebook, Inc. announced what it likely thought was a successful PR coup, namely the funding of privacy research shepherded by two partner organizations, Social Science One and the Social Science Research Council. Not surprisingly, there was no mention that Facebook would be provided specific recommendations from these organizations let alone have such recommendations eventually adopted by the company.

A different sort of threat to Facebook can be found in the decentralized Internet currently being built by start-ups such as Blockstack– which recently filed a SEC Reg A+ offering for $50 million by way of a subsidiary. Blockstack looks to leapfrog centralized platforms such as Facebook by building tools for a “decentralized computing network and app ecosystem” that includes decentralized storage allowing for porting of app data across social media platforms as well as self-sovereign user IDs that would allow for single user identities and passwords across every online application.

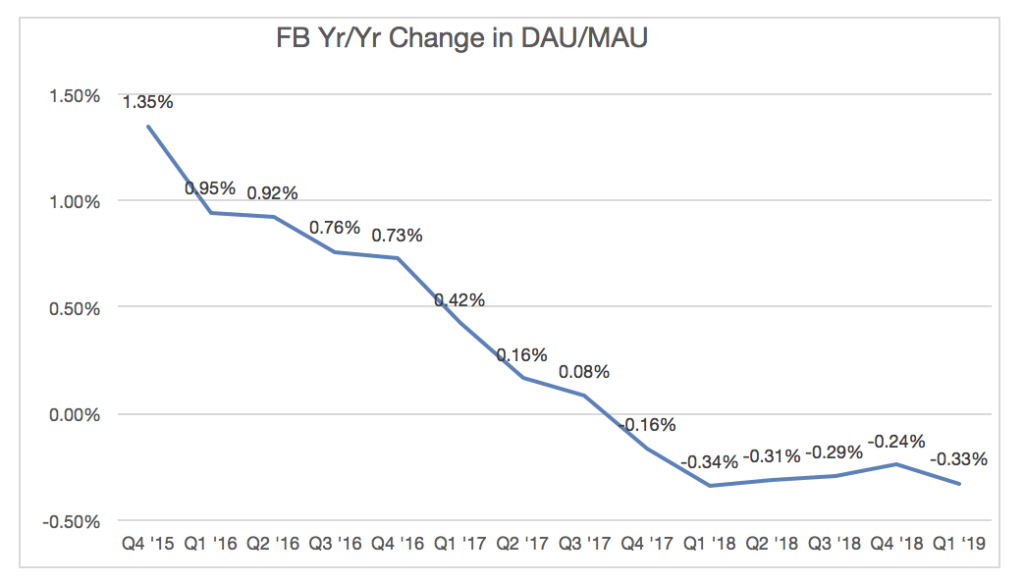

More than likely, however, the most damaging threat to Facebook in the near term is the platform’s continued drop in customer engagement. As recognized by Lou Kerner: “On April 24th, 2019, Facebook reported Q1 ’19 earning, and once again, Wall street applauded, sending the shares up 8%, adding another $45 billion in value. While some saw triumph, and others saw further reason to break Facebook up, all I saw was continued decline in the only metric that matters, engagement.”

Kerner’s graphic on the steady decline of daily and monthly active Facebook users is ominous:

Notwithstanding its many privacy transgressions and current regulatory/litigation challenges as well as the future advent of a decentralized Internet, what likely will be the most direct cause of Facebook’s downfall as a platform stems from the simple fact users have been steadily moving away from using it.

Apparently, users have taken the advice of WhatsApp co-founder Brian Acton and have chosen to “delete Facebook.” Even though Facebook, Inc.’s present cash reserve and its other popular applications would likely allow the company to continue as a viable entity for many years even without its eponymous platform, those present users who spend hours each day on Facebook – and have no desire to ever abandon it, might just not be enough to sustain the Facebook platform in the long term.

Simply put, with shrinking levels of engagement the Facebook platform may eventually go from a MySpace to Vine.

The SEC on April 3, 2019 issued a No-Action Letter to an ICO offeror – demonstrating that its Chairman’s prior promise to devote sufficient SEC resources toward better understanding initial coin offerings has been kept. In the April 2, 2019 no-action request to the SEC, TurnKey Jet proposed, “to offer and sell blockchain-based digital assets in the form of “tokenized” jet cards.” TurnKey plans to be the program manager for a membership program based on this token platform. The tokens would be pegged at the US dollar “throughout the life of the Program”. Apparently, the sole purpose in issuing tokens is to avoid financial transaction costs to the extent a credit card is used to book jet travel.

Even though there is certainly value in eliminating the middleman in high-cost transactions – card brands, Venmo, and Paypal take note, this is not the sort of blockchain-implemented ecosystem envisioned by the early ICO issuers. Nevertheless, this sort of use case provides a readily apparent benefit to its participants and is exactly what the blockchain/DLT community needs to move forward. As previously argued, it is certainly not the case that all ICOs are securities so this no-action move by the SEC should be welcome by all.

In a related positive move from the SEC, on April 3, 2019 the SEC released its Statement on “Framework for ‘Investment Contract’ Analysis of Digital Assets”. Doing an excellent job of parsing the existing statutory interpretation of what constitutes a security, i.e., the now famous Howey test, the SEC’s FinHub Framework is a must-read for those looking to issue a digital asset.

Notwithstanding some criticism of the SEC Framework, this release is a natural progression that should not be discounted. More importantly, by launching this Framework the same day of its No-Action Letter, the SEC has sent a clear message that blockchain ecosystems remain open for business and the SEC will not hurl unnecessary impediments to the implementation of those use cases that actually comply with regulatory law.