Chainalysis discovered ransomware victims paid out in 2020 more than $50 million worth of cryptocurrency to addresses that carried sanctions – with mainstream exchanges receiving “more than $32 million from ransomware strains associated with sanctions risks.” Given the public market embrace of crypto exchanges, it is very likely those exchanges seeking greater regulatory scrutiny will eventually implement curbs to address the OFAC October 2020 advisory – eventually making it more difficult for smaller businesses to satisfy ransomware demands.

On April 17, 2020, it was reported that researchers at Finland’s Arctic Security found “the number of networks experiencing malicious activity was more than double in March in the United States and many European countries compared with January, soon after the virus was first reported in China. ”

Lari Huttunen at Arctic Security astutely pointed out why previously safe networks were now exposed: “In many cases, corporate firewalls and security policies had protected machines that had been infected by viruses or targeted malware . . . . Outside of the office, that protection can fall off sharply, allowing the infected machines to communicate again with the original hackers. “

Tom Kellerman – a cybersecurity thought leader, distills it this way: “There is a digitally historic event occurring in the background of this pandemic, and that is there is a cybercrime pandemic that is occurring.”

While there are certain internal ways of addressing cybersecurity threats arising from a viral pandemic, the exposures now faced by corporations become doubly damaging when the outside resources absolutely necessary to combat active threats are considered off-budget or not a critical enough priority. Smart companies generally survive stressful times by prioritizing with some foresight. Network security during a Cyber Pandemic should be a top priority no matter what size business.

During our Cyber Pandemic, companies recognizing and properly addressing the potential damage caused by threat actors will not only survive minor short-term hits to their bottom line caused by paying outside resources, they will likely be the ones coming on top after both Pandemics subside. There is definitely a light at the end of the tunnel for those willing to take the ride – just continue using trusted vehicles to get you there.

When implementing COVID-19 business continuity plans, companies should take into consideration security threats from cybercriminals looking to exploit fear, uncertainty and doubt – better known as FUD. Fear can drive a thirst for the latest information and may lead employees to seek online information in a careless fashion – leaving best practices by the wayside.

According to Reinsurance News, there has already been “a surge of coronavirus-related cyber attacks”. Many phishing attacks “have either claimed to have an attached list of people with the virus or have even asked the victim to make a bitcoin payment for it.” Not all employees are accustomed to the risks from a corporate-wide work from home (WFH) policy given the previous lack of intersection between work and personal computers.

One cyber security firm released information outlining these WFH risks. And, another security provider offers a common-sense refresher: “If you get an email that looks like it is from the WHO (World Health Organization) and you don’t normally get emails from the WHO, you should be cautious.” In addition to recommendations made by security consultants, there are privacy-forward recommendations that will necessarily mitigate against phishing exploits. For example, WFH employees should be steered towards privacy browsers such as Brave and Firefox to avoid fingerprinting and search engines such as Duckduckgo for private searches. A comprehensive listing of privacy-forward online tools is found at PrivacyTools.IO.

Criminals have already exploited the current FUD by creating very convincing COVID-19-related links. As reported by Brian Krebs, several Russian language cybercrime forums now sell a “digital Coronavirus infection kit” that uses the Hopkins interactive map of real-time infections as part of a Java-based malware deployment scheme. The kit only costs $200 if the buyer has a Java code signing certificate and $700 if the buyer uses the seller’s certificate.

At a very basic level, WFH employees should be reminded not to click on sources of information other than clean URLs such as CDC.Gov or open unsolicited attachments even if they appear coming from a known associate. Now that banks, hotels, and health providers are sending emails alerting their clients of newly-implemented COVID-19 procedures, it is especially easy to succumb to spear phishing exploits – which is the hallmark of state-sponsored groups. As recently reported, government-backed hacking groups from China, North Korea, and Russia have begun using COVID-19-based phishing lures to infect victims with malware and gain infrastructure access. These recent attacks primarily targeted users in countries outside the US but there should be little doubt more groups will focus on the US in the coming weeks. Until ramped up testing demonstrates that the COVID-19 risk has passed, companies are well advised to focus some of their security diligence on these targeted attacks.

The CDC reports in its latest published statistics there were 802,583 reported cases of COVID-19 and 44,575 associated deaths. Without a doubt, this pandemic is certainly much worse that the Swine Flu pandemic as previously reported by the CDC. Moreover, the current “panic pandemic” certainly shows no indications of subsiding.

On April 30, 2020, it was reported Tonya Ugoretz, deputy Assistant Director of the FBI Cyber Division, stated the FBI’s Internet Crime Complaint Center (IC3) is currently receiving between 3,000 and 4,000 cybersecurity complaints daily – IC3 normally averages 1,000 daily complaints.

UPDATE: May 6, 2020

On May 5, 2020, a joint alert from the United States Department of Homeland Security Cybersecurity and Infrastructure Security Agency and the United Kingdom’s National Cyber Security Centre warned of APTs targeting healthcare and essential services.

The alert warned of “ongoing activity by APT groups against organizations involved in both national and international COVID-19 responses.” This May 5, 2020 alert follows an April 8, 2020 Alert that warned in broader terms of malicious cyber actors exploiting COVID-19.

APTs are conducted by nation-state actors given the level of resources and money needed to launch such an attack. Moreover, they generally take between eight and nine months to plan and coordinate before launching. It is particularly disheartening that these recent attacks include those launched by state-backed Chinese hackers known as APT 41. As one cybersecurity firm points out in a recently-released white paper: “APT41’s involvement is impossible to deny.”

Distilled to its essence, the uncovered APT41 attacks mean that before COVID-19 was even on US shores, Chinese state-actors were planning attacks targeting the healthcare and pharmaceutical sectors. One can only hope the cyberattacks were not coordinated alongside the spread of the virus – a virus that only became public months after a coordinated attack would have been first planned.

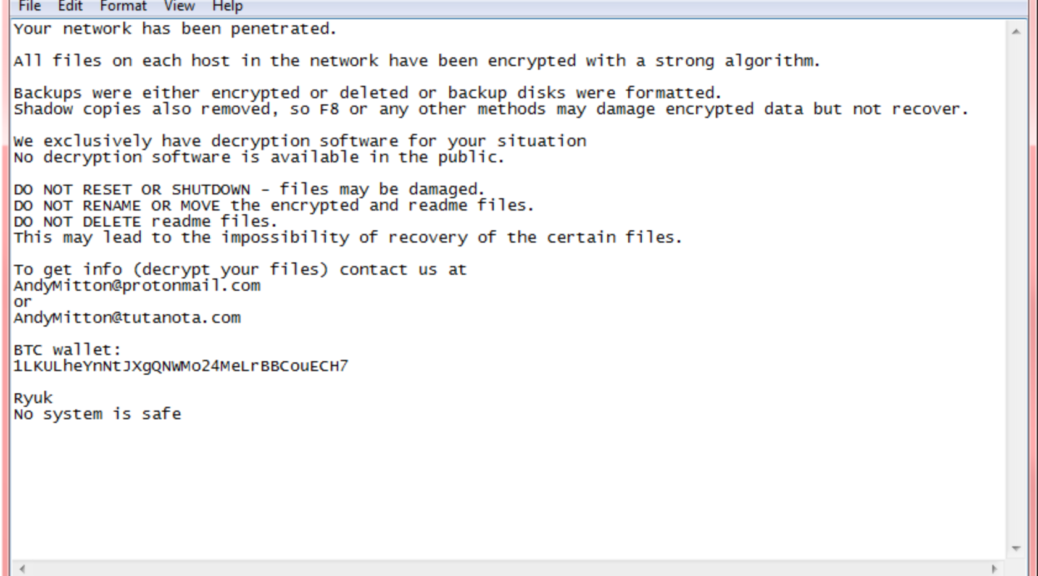

Even though the first significant uptick in ransomware attacks began over three years ago, a steady increase in frequency and severity has likely now made ransomware exploits the number one security threat faced by most businesses today. McAfee places the ransomware growth rate for the last quarter at 118%. Many smaller businesses were previously on notice but chose to ignore the warning signs. Thankfully, after the 2017 ransomware attacks unleashed by the Wannacry strain of Cryptolocker, some companies did address ransomware risk by implementing better employee training while others decided to upgrade legacy software and initiate offsite backups.

Those who did not adequately address this risk, however, are now facing much larger extortion demands. Also, the risk landscape has changed dramatically over the past several years with ransomware becoming an equal opportunity attack that will now target local governments as well as dental offices. Indeed, even first grade students are now being impacted by network security intrusions that not too long ago only previously targeted only large universities.

Despite the recent public trend of paying these extortion demands, the FBI has long advocated not paying a ransom in response to a ransomware attack. Specifically, the FBI has said: “Paying a ransom doesn’t guarantee an organization that it will get its data back—we’ve seen cases where organizations never got a decryption key after having paid the ransom. Paying a ransom not only emboldens current cyber criminals to target more organizations, it also offers an incentive for other criminals to get involved in this type of illegal activity. And finally, by paying a ransom, an organization might inadvertently be funding other illicit activity associated with criminals.”

In fact, some have argued that by having insurance for this exposure the industry itself is actually at the root of increased ransomware activity. Those in the security industry correctly point out that what drives these actors turns more on quick conversion rates rather than whether an insurer stands behind a victim. To suggest the insurance industry is the cause of this problem gives threat actors way too much credit while completely ignoring the benefits derived from the cyber insurance underwriting process.

In the same way it is never too late to go back to school, it is never too late to begin importing a more robust security and privacy profile into an organization – which is the only real way to diminish the risk of a ransomware attack. As suggested in 2016: “Given the serious threat of ransomware, businesses large and small are reminded to at least do the basics – train staff regarding email and social media policies, implement minimum IT security protocols, regularly backup data, plan for disaster, and regularly test your plans.”

First introduced by Sen. John Thune, The Red Flag Program Clarification Act of 2010, S. 3987, would define a creditor as someone who uses credit reports, furnishes information to credit reporting agencies or “advances funds…based on an obligation of the person to repay the funds or repayable from specific property pledges by or on behalf of the person.” Sen. Thune’s web site statement regarding the regulations states that action was necessary given the FTC was threatening small businesses with its regulations.

As written, the existing law applies to “creditors,” a term the FTC interpreted broadly to include professionals who regularly deferred payment on services. The FTC had delayed enforcement of these regulations numerous times due to pressure by the ABA and AMA given that the sweeping nature of the regulations would take into account professionals who would incur significant costs to address a perceived slight exposure. As recognized on the House floor by Rep. John Adler (D-N.J.),“When I think of the word ‘creditor,’ dentists, accounting firms and law firms do not come to mind.”

Lost on many is the fact these regulations will remain in force and will still impact business owners throughout the country, including financial institutions, car dealers, contractors, utilities, phone providers, retailers (if financing is provided), mortgage brokers, etc. Moreover, even if a business may no longer be “technically” within the rubric of the regulations, it may be a good best practice to still comply. For example, an ID theft victim may look to the FTC Red Flags regulations to help determine a baseline reasonableness standard. Although estimates of compliance costs range from $1,000 to $1,500 for small business owners, this amount may pale when compared to the expenses incurred in defending a data breach claim.

In a recent National Law Journal article, Adrian Dayton argues that smaller law firms have been much better at jockeying for online positioning and expanding their digital footprint. Driven by the ultimate goal of search engine optimization (SEO), these firms have been using blogs, FaceBook, Twitter and LinkedIn to get noticed in ways the largest firms are not.

As pointed out by the author, run a Google search for “class action defense”and you will notice that the top listing is a blog produced by the law firm of Jeffer Mangels Butler & Mitchell — a firm with three offices and 138 attorneys. Given its blog, the firm dominates in SEO despite being relatively small. Google’s search algorithms, including its PageRank methodology, place a premium on the sort of fresh content found on blogs. Search results slanting in favor of smaller law firms pretty much run across the board given “the fact that in the entire AmLaw 100 there are more than 84,000 lawyers and only 130 law blogs.” Not much in the way of competition. In other words, if you want to get up in the rankings and get noticed by new clients looking for your perspective on legal matters, having a blog has been the quickest path to achieving that goal.

Why does any of this matter?

Well, according to a Greentarget/ALM survey, 35% of in-house counsel had visited a law blog within the past 24 hours and forty-three percent of in-house counsel cited law blogs among their top “go-to” sources for news and information. This sort of “drip marketing” may take law firms months or even years to obtain an engagement given the strong existing relationships that first need to be shaken loose. On the other hand, it is likely the most cost-effective way to get the ball rolling.

Given free publishing tools such as WordPress coupled with inexpensive professional themes and low-cost hosting options, the only real cost is the time it takes to write the blog post. If you are a competent brief writer, it should take you no more than 30 minutes of your time every few days. And, as correctly pointed out by Adrian Dayton, this small time commitment is well worth it. Try it. You may even enjoy the experience. Just make sure what you write is not something that will impact a client relationship — after all, that is likely the reason larger firms have generally stayed away from the blogosphere.

It’s been six months since passage of the administration’s healthcare reform act — the Patient Protection and Affordability Care Act (PPACA). As reported in newspapers around the country, that means that for those health plans that begin today:

Parents will be able to keep their young adult children on their group health plan up to age 26, regardless of whether the adult child lives with the parent, is a full-time student, disabled or married.

Insurance companies will be banned from dropping coverage when an enrollee gets sick.

All new plans must offer free preventive services, such as mammograms, colonoscopies and certain child preventive health-care services, meaning plans can’t charge deductibles, co-pays or co-insurance.

All employer plans and new plans in the individual market will be prohibited from denying coverage to children under age 19 with pre-existing conditions.

Parents will be able to select a pediatrician as the primary care provider for their children.

Female enrollees will be able to obtain obstetrical/gynecological specialist services without a referral from another primary care provider.

Group plans will be banned from imposing lifetime benefit limits and will start gradually eliminating annual benefit limits.

New plans must provide consumers access to an internal and external claims appeals process.

For plans operating on the calendar year, these new PPACA requirements will take effect on January 1, 2011.

This past May, SAP and Waste Management announced the settlement of a lawsuit involving a failed ERM implementation. Waste Management sued SAP for fraud in March 2008 over an allegedly failed waste and recycling revenue management system. Waste Management allegedly sustained direct damages of over $100 million. SAP responded in its original Answer that Waste Management didn’t “timely and accurately define its business requirements” nor provide “sufficient, knowledgeable, decision-empowered users and managers” to work on the project. Much of Waste Management’s allegations turned on representations made by salespersons who were allegedly only concerned about licensing software that would create larger year-end bonuses. According to its revised complaint, if a newer version had been used, “the multi-million dollar sales price for the software could not be immediately recognized as revenue under the accounting rules for revenue recognition,” and those salespeople involved in the deal would not receive bonuses. According to its quarterly earnings filing regarding the reported settlement, Waste Management received “a one-time cash payment” in accordance with the settlement. The terms of the settlement were not disclosed.

The price of a tech suit goes down steeply after fraud charges are dismissed. For example, a lawsuit brought by a county government went from $10 million in alleged damages to an eventual settlement of $575,000 given there were only breach of contract claims remaining after the fraud claims were earlier dismissed from the action. Another action brought by yet another county government may not go as well for the tech vendor (Deloitte Consulting) given the fraud claims remain front and center throughout the complaint filed on May 28, 2010.

Claims are not only brought against tech vendors for millions of dollars. Last year, Epicor was sued after a client spent $244,656.42 on an ERP implementation. Again, the complaint sounded in contract breach but had negligent representation as well as fraud claims. Here’s a list of similar suits.

Moreover, tech vendors can include those who sell products such as iPhones rather than license software. Earlier this month, Apple was hit with numerous suits seeking damages arising from the fact the latest iPhone has significant reception issues depending on how the phone is held. Specifically, one suit accuses Apple of “general negligence, breach of warranty, deceptive trade practices, intentional misrepresentation, negligent misrepresentation, and fraud by concealment.”

For over twenty-five years, courts have allowed fraud claims to mingle with the negligence and breach of contract claims typically brought against technology vendors. It is so much easier to prove (as was done in the EDP suit) that someone lied when contracting as opposed to showing how a contracted for systems implementation was not technically performing as promised. Moreover, if fraud is proven, it will not only vitiate the limitation of liability and exclusion of consequential damages found in nearly all tech agreements, punitive damages may also become available. In other words, a fraud claim is the magic bullet used by most plaintiffs to go around iron-clad contracts and the bar against awarding punitive damages in a contract dispute.

To best combat fraud claims, there are certain things that a tech vendor should do before, during and after a contract is negotiated. For counsel on that front and for access to related risk management and contracting tools, please reach out.

Claims arising out of internally-used software continue to be a significant retained IT risk factor. When President Obama picked the Business Software Alliance’s General Counsel Neil MacBride for a senior Justice Department post, it was a clear message that we will see increased software compliance audits – and possible new penalties. The increasing use of open source software is also leading to unanticipated software copyright exposures. In other words, the reasons continue to mount why users of desktop software should carefully monitor their use of software and maintain careful records of each license.

Taking advantage of a federal law passed last year, Connecticut’s Attorney General, Richard Blumenthal, announced yesterday a settlement with HMO Health Net that includes a corrective action plan, a $250,000 payment to the State of Connecticut (with an additional potential pot of $500,000), and increased credit monitoring and ID theft insurance to potential victims. According to Blumenthal’s original lawsuit, Health Net lost or had stolen a disk drive last year containing sensitive information from 1.5 million persons – including 446,000 Connecticut residents. The drive contained names, addresses, social security numbers, HIPAA-protected health information and financial information.

The underlying federal statute relied upon by Blumenthal when bringing suit against Health Net is Title XIII of the American Recovery and Reinvestment Act of 2009, also known as the Health Information Technology for Economic and Clinical Health Act (the HITECH Act). The HITECH Act not only offers financial incentives to prod the use of electronic health records (EHR) but also greatly expands the protections afforded such information. For example, it creates the first federal breach notification law. Covered Entities and Business Associates that “access, maintain, retain, modify, record, store, destroy or otherwise hold, use or disclose” unsecured personal health information must disclose to the owner notice of a breach. SeeSections 13402(a) and (b) of the HITECH Act.

In obtaining yesterday’s settlement, Blumenthal was the first Attorney General to take advantage of the HITECH Act’s grant of HIPAA compliance jurisdiction to state Attorney Generals. It is entirely likely that other states will now jump on this bandwagon – especially those with AGs seeking higher political office. In fact, last month AG’s from across the country were scheduled to receive training on HIPAA compliance from Booz Allen Hamilton.

As for the Health Net settlement, the amounts paid to Connecticut are small compared to what has been spent to date dealing with the breach. According to the settlement agreement, Health Net allegedly has already spent more than $7 million to investigate what happened to the disk drive, notify members and provide credit monitoring and identity-theft insurance to those potentially impacted. It is incidents like these that showcase the value of requiring strong indemnification language backed by an equally strong requirement of data breach insurance coverage for those firms managing or holding your patients’ or members’ sensitive medical information.